Early consideration of the expected social security values for the coming year is of interest for business planning. We will provide you with the expected values for 2026.

AttentionPursuant to Section 810 para. 3 ASVG, the low income threshold for 2026 remains „frozen“ (as does the threshold derived from it for the flat-rate employer contribution). The other values will increase in line with the revaluation figure of 1.073.

Accordingly, the following social security values are expected to apply for the 2026 calendar year:

- Low income threshold per month: EUR 551.10 (unchanged compared to 2025)

- Threshold for the flat-rate employer contribution: EUR 826.65 (unchanged from 2025)

- E-Card service fee: EUR 26.85 (effective date 15/11/2026)

- Maximum contribution base:

- monthly: EUR 6,930.00

- daily: EUR 231.00

- Maximum annual contribution base for special payments: EUR 13,860.00

- Maximum monthly contribution base for freelance employees without special payments: EUR 8,085.00

- Limit amounts for unemployment insurance-low pay:

- up to EUR 2,225.00: 0 %

- over EUR 2,225.00 up to EUR 2,427.00: 1.00 %

- over EUR 2,427.00 up to EUR 2,630.00: 2.00 % (apprentices 1.15 %)

- over EUR 2,630.00: 2.95 % (apprentices 1.15 %)

As usual, the final confirmation by the ÖGK and the announcement in the Federal Law Gazette remain to be seen.

Update wage garnishment values

It was recently determined that pensions for 2026 - apart from caps for certain higher pensions - will be increased by 2.7 % (adjustment factor 1.027). Accordingly, the minimum pension (equalisation supplement reference rate for single persons) will increase from EUR 1,273.99 to EUR 1,308.39 with effect from 1 January 2026.

As the minimum subsistence level is derived from the minimum pension, the following wage garnishment values are expected to apply from 2026:

| Living wage values 2026 (expected) | monthly | weekly | daily |

| General basic amount | 1.308,00 | 305,00 | 43,00 |

| Increased general basic amount | 1.526,00 | 356,00 | 50,00 |

| Basic maintenance amount | 261,00 | 61,00 | 8,00 |

| Maximum calculation basis | 5.220,00 | 1.220,00 | 174,00 |

| Absolute minimum living wage - with normal seizure - in the case of maintenance seizure | 654,00 490,50 | 152,50 114,38 | 21,50 16,13 |

Formal confirmation of these values by the BMJ is still pending.

November update

- Pension settlement: The threshold amount for the application of preferential taxation of pension settlements (half tax rate) will increase from EUR 15,900 to EUR 16,500 from 1 January 2026.

- Interest on arrears in social insurance: The interest rate for interest on arrears in social insurance contributions is to fall from 1 January 2026 from % 7.03 to % 5.53.

- Transport deduction (annual): EUR 496.00, increased transport tax credit EUR 853.00 (thresholds: EUR 15,069.00 to EUR 16,056.00), supplement to the (increased) transport tax credit EUR 804.00 (thresholds: EUR 19,761.00 to EUR 30,259.00).

- Pensioner deduction (annual): EUR 1,020.00 (maximum deduction limits: EUR 21,614.00 to EUR 31,494.00), increased pensioner deduction EUR 1,502.00 (maximum deduction limits: EUR 24,616.00 to EUR 31,494.00).

- Deductions: The single-earner deduction and the single-parent deduction, the transport deduction and the pensioner deduction will be adjusted as follows as of 1 January 2026:

- AVAB/AEAB (annual): one child EUR 612, two children EUR 828, each additional child an additional EUR 273

- Additional income limit for AVAB (partner income): EUR 7,411.

Income tax

The Inflation Adjustment Ordinance will result in these income tax rate brackets in 2026:

| Income components (annual) | Tax rate |

| up to EUR 13,539.00 | 0 % |

| between EUR 13,539.00 and EUR 21,992.00 | 20 % |

| between EUR 21,992.00 and EUR 36,458.00 | 30 % |

| between EUR 35,458.00 and EUR 70,365.00 | 40 % |

| between EUR 70,365.00 and EUR 104,859.00 | 48 % |

| between EUR 104,859.00 and EUR 1 million. | 50 % |

| over EUR 1 million. | 55 % |

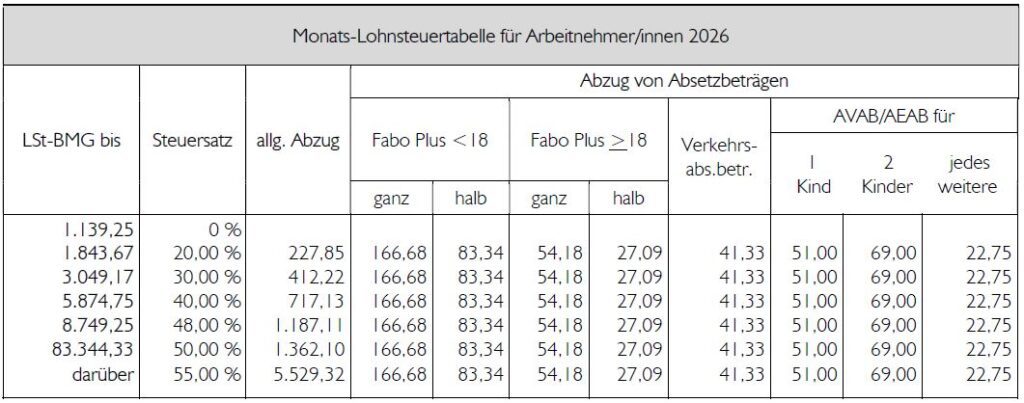

Wage tax table 2026

Definitive effectiveness is achieved through official confirmation by the BMF.

Status: 03.11.2025

Created: 03.09.2025

Source: Kraft & Kronberger specialised publications

Photo: Cup of Couple